Understand the facts around a loan commitment letter and how to use one to win a bidding war to buy a home

The home buying market is hot and you’re locked in a bidding war for your dream house. You put in an offer that’s a few thousand above the rest and expect to win out…and then find out the seller picked someone else! What gives?

It might be that the other buyer had a loan commitment letter. This letter from your lender can be a powerful weapon in the war to win a bid. It assures sellers that financing is in place and closing will go smoothly.

So what is a loan commitment letter exactly? Does it guarantee you’ll get a loan and how do you get one from your lender?

What is a Loan Commitment Letter?

A loan commitment letter is provided by a mortgage lender to say that a borrower has passed underwriting standards to qualify for a loan. It’s a stronger guarantee than a simple pre-approval letter from a loan officer because it involves a deeper look into your credit.

Getting a loan commitment letter is a great way to assure sellers that you’re serious about buying their home and can help you win in a bidding war with other buyers. I’ve seen buyers accept a borrower offering less than others because they had a commitment letter for financing.

It’s important to understand that a commitment letter doesn’t guarantee you a loan though. There are usually conditions within the letter you’ll need to meet.

Is a Loan Commitment Letter Legally Binding?

Mmmm, not really. On the borrower side, you’re not bound to taking a loan from the lender. It might mean losing any fees you paid to get the letter but you can always go with another lender and a better interest rate.

On the lender side, a commitment letter is more binding but there’s still some wiggle room. Commitment letters usually include conditions that have to be satisfied before you get a loan. For example, it may state that you must keep your job and have no significant changes to your credit before closing.

Changes that can void a commitment letter include:

- Big changes in your credit score caused by defaults or derogatory marks

- Loss of your job

- Low property appraisal

- Change in your cash amount for down-payment

These aside, a loan commitment letter is almost always honored by the lender. Sellers can ask for conditions to be removed and some lenders will comply.

Loan Commitment Letter vs Pre-Approval

Most buyers are more familiar with a pre-approval letter and there’s some confusion between the two. A loan pre-approval is given to you by the loan officer after a basic look at your credit report and income. The loan officer will look at your credit report, types and amounts of debt you owe, down-payment and verify your income.

A pre-approval letter is a first step in getting your loan or showing sellers you’ve got financing but it’s no guarantee. The process is faster than a commitment letter but doesn’t include some important steps needed before you’re actually approved for a loan.

A loan commitment letter is issued after your credit has been approved by underwriting, which is the department with final say on your loan. It involves a deeper look at your credit and will take longer but almost guarantees you’ll be approved when you need the money.

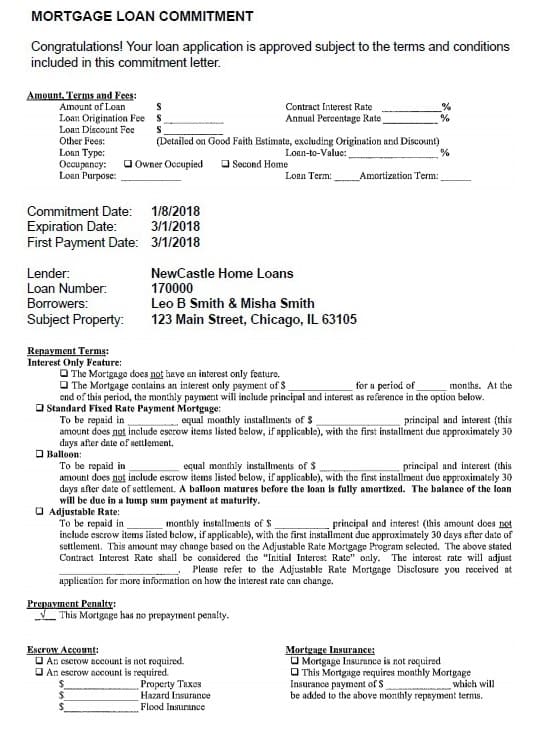

Loan Commitment Letter Sample

Loan commitment letters will vary depending on your lender. Some look more like letters, congratulating you on getting the loan and talking through the points. Others will be much more like a jumble of numbers, spelling out the proposed loan.

Whatever form your commitment letter takes, there are a few things you need to verify and check before accepting it.

- Make sure the loan amount is correct

- Check for different fees including origination, application and underwriting

- Check the interest rate and annual percentage rate (APR)

- Review your loan type, i.e. fixed or variable rate

- Check the expiration date on the loan commitment

Getting a loan commitment letter is the one of the best ways to show sellers you’re serious about buying a home and can put you ahead of others in a bidding war. It all but guarantees you financing for a mortgage but will come with a few fees. Make sure you understand the terms around your loan and know that you’re never locked into a lender until signing on your mortgage.