Don’t miss out on a big income tax refund and get to know the 2018 tax changes that will get you that check

Tax season is here and this year promises to be more confusing than ever, as if it was possible for income taxes to be more confusing.

While some people may be getting a bigger refund on their taxes this year, you’ll need to know where to find it. From income tax rates to deductions and other loopholes, a lot has changed for filing your 2018 taxes.

I’m listing here the top five changes to income taxes that will help you get the biggest refund possible and how to make filing easy. Whether you do your own taxes through an easy tax software product or have an accountant handle the mess, don’t miss out on what could be thousands back from Uncle Sam.

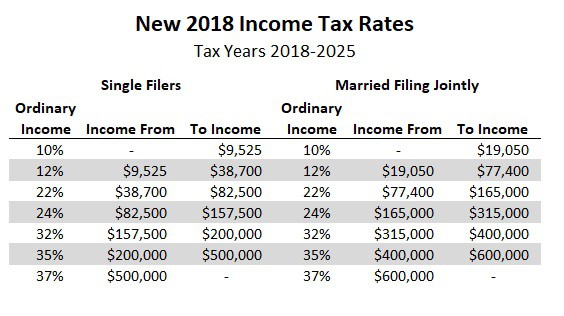

2018 Income Tax Rate Changes

The biggest change on income taxes is the rates and brackets. The lowest rate is still 10% but most of the other brackets came down a few percent and the top income in each tax bracket increased a little.

It might not seem like much but every bit helps in boosting your tax refund. For example, a married couple making an adjusted gross income (AGI) of $65,000 in 2017 would have owed about $8,817 to federal taxes. This year, they’ll owe a slightly lower $7,419 for more than a grand in savings.

The change in the overall tax rates for 2018 will stay in effect until 2025 but are then set to return to the old, higher levels. Politicians are promising to make the new tax rates permanent…but do you really want to trust them on it?

Now might be a good time to start contributing to your Roth IRA since income taxes are lower. You won’t get the immediate deduction you get contributing to a traditional IRA but you won’t owe taxes when you withdraw your money in retirement.

Want to make filing taxes as easy as possible? I use TurboTax to file every year and always get a refund. Whether you’re filing for your family or are a small business owner like myself, TurboTax will walk you step-by-step to getting the biggest refund possible.

Click Start your taxes for free and get the TurboTax Guarantee

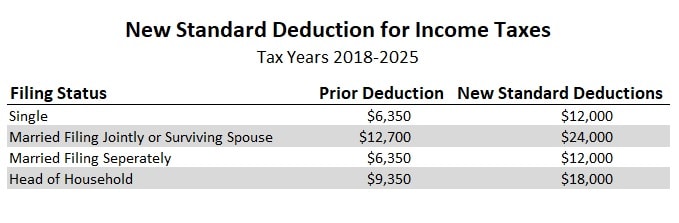

The 2018 Standard Deduction is Higher

When you file your taxes, you can either take a flat amount off your income and then pay income taxes on the rest, or you can add together all your individual deductions in a process called itemizing.

Those individual deductions include things like state and local taxes, interest and charitable donations. For those in high-tax states, it used to make more sense to add up and itemize because property taxes were higher than that standard deduction they could take.

That’s all changing for the new tax law because the standard deduction increased big time. In fact, the flat amount you can take off your income almost doubled.

Unfortunately, it also means the return on some of those itemized deductions might not mean as much. If you were trying to decide how much those charitable contributions really cost after taxes, that math has changed. If those individual deductions no longer add up to more than the standard deduction you can take, then you’re better off just taking the flat amount.

But Many of the Smaller Deductions are Gone for 2018 Taxes

Before you get too excited about the new lower tax rates and the higher standard deduction, there are a few parts of the new tax law that will increase your taxes.

In previous years, you could deduct ‘miscellaneous deductions’ which included things like safe deposit fees, investment management, union dues and unreimbursed employee expenses if they added to more than 2% of your AGI.

That deduction has disappeared from the 2018 tax law and will particularly hit workers in unions that have to buy some of their own tools. This could include anyone in public safety as well as construction.

The Personal Exemption is also Gone for 2019 Tax Filing and Beyond

The higher standard deduction is great but it didn’t come without a cost. In previous years, you could take an additional $4,050 off your income for yourself, your spouse and any dependents. It was a benefit to people that itemized as well as those that took the standard deduction.

You no longer get that personal exemption which can be a big hit to larger families. In fact, for families of four or more, the disappearing personal exemption means you’re worse off when you go to file your taxes.

State and Local Tax Deductions are Capped at $10,000 on the New Tax Law

If you never needed to itemize your individual deductions then this one might not be such a big deal. For example, those living in low-tax states that rented their homes had fewer deductions and the standard deduction was almost always higher.

For homeowners in high-tax states though, this new tax law change could hit them hard. In fact, we’re already hearing of a migration of people moving from states like New York and California to places in Florida and Nevada.

In prior years, you could take all the taxes you paid to local and state government off your federal income taxes. That meant a lot for people paying thousands in property taxes and mortgage interest…so homeowners.

In 2019 and beyond, you will only be able to take a maximum of $10,000 off your federal income taxes for the amount paid to state and local taxes. That’s the limit for single or married filing jointly. Married people filing separately have a $5,000 cap each.

The change will most likely affect those living in higher-tax or higher cost-of-living states like those in the New England states or the west coast.

Try TurboTax for Free to See How Much You’re Getting Back this Year

The new tax laws will take some time to understand but don’t let that get in the way of getting a big refund. Use these five tax law changes to get as much back as possible. Understand the 2018 income tax changes weren’t all good so you’ll need to work your way around them to get the most benefit and avoid the worst of the pain.