See how to get a good interest rate on any type of loan and what it means for your payments

More than four million Americans live in a house they can’t afford. Seven million borrowers are more than three months behind on their car loan. These people live under a cloud of stress and anxiety that darkens every day of their life.

The difference between a good interest rate and a bad one will change your life.

I know. I lived the nightmare in 2009 after destroying my credit score. My FICO plunged from 800 to 560 in a matter of months and interest rates on loans jumped. With each increase in interest rates, I fell deeper and deeper into debt I couldn’t afford.

That’s why I wanted to take a look at interest rates, what makes for a good interest rate on a loan and give you some pointers on how to get the best rate possible.

What is APR on a Loan?

First off, it’s important to know the difference between the interest rate and the APR you hear so much about.

The interest rate on your loan is going to be the rate quoted when you get the loan. That’s the rate the loan officer is going to tell you or you’ll see when you fill out an online application.

The APR or annual percentage rate is your actual cost of the loan. You hear about this other rate because it’s required by law that lenders show you on your loan documents. The APR is the interest rate you’re actually paying when you include all the fees on the loan.

Most of the time, the APR and interest rate will be so close that it doesn’t really matter. In that case, you can compare the APR or interest rate across loans. When it matters is when the APR is much higher than the interest rate the loan officer is quoting you, like when the APR is more than half a percent higher.

This could be a warning signal that loan fees are too high for your loan. When this happens, make sure you shop your loan around to make sure you’re not getting taken advantage of by lenders with super-high fees.

Lenders compete for your loan on PersonalLoans – check your rate for up to $35,000

Why is My Interest Rate Important?

Well, interest rate is important because that’s the cost of your loan. That cost of the loan is what gets most people in trouble when it comes down to paying off the debt.

For example, the difference in monthly payments on a $24,000 car loan over 60 months is $50 a month for a 8.5% interest rate versus 4% loan. That might not seem like much of a difference until you consider the monthly payments of $492 for the 8.5% loan and $442 for the 4% loan.

When you’re talking about large loans, even the smallest change in interest rate can mean the difference between making payments and falling into bankruptcy.

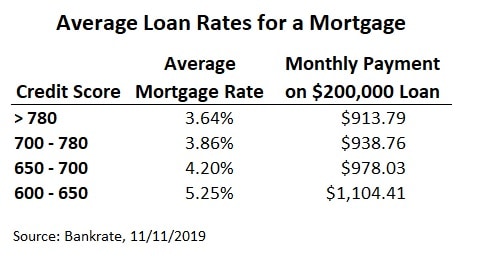

What is a Good Interest Rate on a Mortgage?

A good interest rate depends on what type of loan you’re talking about so I’ll cover the three most common loans; mortgages, personal loans and car loans. This will help you compare your loan offers when you fill out an application.

Understand that loan rates change constantly depending on other rates but these rates are all current.

Interest rates on mortgages are the lowest you’ll find. That’s because the bank can foreclose on your home if you don’t make payments. It’s a secured loan versus the unsecured-type of debt like we’ll see with personal loans.

Most lenders will only loan you up to about 80% of the value of your home. That means if they do need to take the home, they’ll usually be able to sell it quick and for a discount while still getting repaid on the loan.

Current rates on mortgage loans range from about 5.25% to 3.6% for really good credit borrowers. You’ll notice that the bottom range for rates only goes to a 600 FICO score. Most lenders won’t even consider a borrower with a credit score below this point.

What is really important about this table is the difference in payments on a $200,000 mortgage loan. Just a one percent difference in interest rate, maybe by increasing your credit score a few dozen points, can save you over $126 a month. That adds up to a savings of $45,500 over a 30-year mortgage loan!

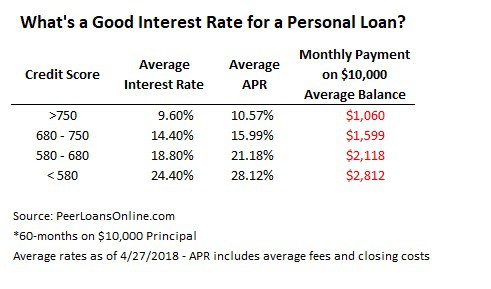

What is a Good Interest Rate on a Personal Loan?

Personal loans and peer-to-peer loans are both unsecured. That means, unlike mortgages or car loans, the lender doesn’t have any kind of collateral on the loan to repossess if the borrower stops making payments.

That means more risk and higher loan rates on these loans.

Considering it’s a loan you get just on your promise to repay, interest rates are actually pretty good though. Rates range from an average around 29% for very poor credit borrowers to just over 6% for good credit borrowers.

What this table doesn’t show is the difference in interest rate by size of the loan or other loan terms. We’ll get into that a little later when I show you how to get the lowest interest rate possible.

Looking at the rates on personal loans and you start to understand why debt consolidation is the top reason people use these loans. A good interest rate on a personal loan is way below the average credit card rate for most people. It just makes sense to borrow on a peer-to-peer loan to pay off that higher-rate credit card debt.

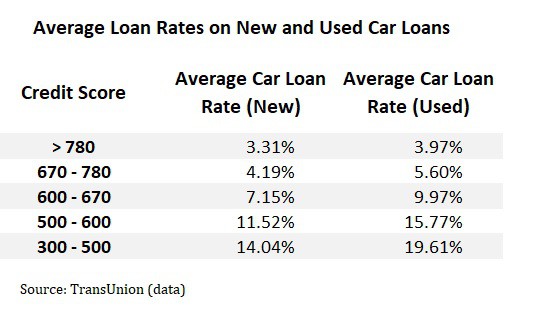

What is a Good Interest Rate on a Car Loan?

Like a mortgage, car loans are secured against the value of the car. That means lenders have some safety in being able to repossess the car and loan rates are generally lower than personal loans.

The big difference here is between the rate you’ll pay on a new car versus a used car loan.

This is a trick of the car dealers. Financing and the interest they collect is the highest profit point for a dealer, way beyond the price markup on cars. Dealers are willing to lower the rate a little if they can get you hooked into a $20,000 new car versus an $8,000 used car.

Car loans are one of the top reasons people give when they file bankruptcy. I’m not saying this to mean you can’t have a nice car but just be careful when signing for that loan. Even a good interest rate on a car loan can mean hundreds of dollars in interest on top of that car payment.

How to Get a Good Interest Rate and Save Money

Getting the best possible interest rate means managing the three factors that control how much lenders charge on the money; credit score, size of the loan and terms of the loan.

Improving your credit score can take a year or longer but even little changes can help you shave a percent or two off your interest rate. If you’re having trouble getting an interest rate you can afford, I recommend a couple quick solutions.

- Use a debt consolidation loan to pay off your credit cards. Pay this small loan back within a year and your credit score will jump.

- Borrow just as much as you need for six months and make payments on the loan. Lenders approve these short-term loans even on bad credit and the payments will help build your credit history.

Most borrowers don’t realize how important the size of their loan is to the interest rate they pay. It’s intuitive if you think about it though. The cost of the loan, the interest rate, is a compensation for the lender taking the risk that the loan will go unpaid.

More risk means a higher interest rate.

Personal loans are available for up to $40,000 on some platforms but most fall within the range of $3,000 to $12,000 with an average around seven grand. The risk that someone will not pay a $40,000 loan is much higher than someone with a smaller $3,000 loan.

The best interest rates you see on peer-to-peer and personal loan sites are usually for loans of $2,500 or less though you can still get these if you have good credit. If you’re trying to get a loan on bad credit though, it’s best to borrow as little as possible.

Just like with the loan amount, the time you need to repay the loan is also a big factor in the interest rate. A loan with payments stretched over 72 months is much riskier than one where the loan is scheduled to be fully repaid over 12 months.

A lot can happen in 60+ months and lenders want to be sure they are compensated with a higher rate for the risk.

While you might not be able to do much immediately about your credit score, you can affect these other two factors to lower your interest rate on a loan.

- Borrow only as much as you need and for the shortest term you can afford. Monthly payments will be higher for shorter-term loans so make sure you can afford the payments.

- If you’re still unable to get a loan you can afford with the trick above, try getting a starter loan for a few thousand and with one-year loan terms. By the time it’s repaid, your credit score will be higher and most platforms give preferential rates to repeat borrowers.

Check your rate on a personal loan now – instant approval!

Getting a good interest rate starts with knowing the factors that affect your rate on different loans. A good rate on one type of loan might be too high on another so make sure you know what rates are in your area. Make sure you also shop your loan around, applying at a few different lenders before you accept one. It won’t take more than a few extra minutes and you’ll know you’re getting the best rate available.