The difference between a good FICO score and bad credit can cost you thousands!

A bad credit score will cost you over $70,000 in extra interest payments on a mortgage…and that’s if you even get approved. But what is a good credit score and how does that loan officer decide whether to greet you with a smile or slam the door in your face?

In this video, I’ll not only show you the difference between a good FICO score and bad credit, I’ll show you the average credit score by age and the score you need to buy a house. I’ll then reveal three credit score hacks I guarantee you’ve never heard and that will increase your FICO fast!

![What is a Good FICO Score? [and 3 Steps To Get One Fast!]](https://i.ytimg.com/vi/QuAN3e9KwNk/hqdefault.jpg)

We’re building a huge community of people ready to beat debt, make more money and make their money work for them. Subscribe and join the community to create the financial future you deserve. It’s free and you’ll never miss a video.

Join the Let’s Talk Money community on YouTube!

More Americans with Bad Credit

So I just saw a report out of the New York Fed that as many as 60 million Americans are locked out of the financial system, unable to get access to credit or the money they need. Now that’s twice as many people as the Fed previously thought and it all has to do with the banks and their requirements around credit score.

So what I wanted to do with this video is answer one of the most common questions I get on the channel, What is a good FICO score and how to get one. We’ll start by looking at the FICO credit score, what makes a good or bad score. Then I’ll show you the average credit score by age to see where you stand.

We’ll dig into the numbers to see what kind of a credit score you need to buy a house or a car and then I’m going to reveal three hacks to boost your score as much as 100 points fast.

What is a Credit Score?

Now your credit score is just a number based on everything in your credit report. The FICO company looks at each of your credit reports from TransUnion, Experian and Equifax, and then scores you based on things like payment history, how much debt you owe and bad marks like late payments, defaults and bankruptcies.

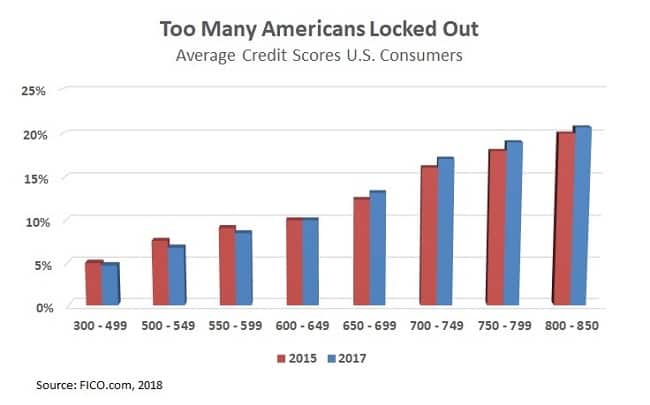

That FICO score ranges from 300 to 850 with about half the population up around 700 FICO or higher. Here I’ve taken data from FICO to show the percentage of Americans within credit score ranges, both for 2015 and the most recent released 2017.

You see about 55% have a score of 700 or above with another one-in-four Americans in the middle here with a score between 600 and 700 FICO. What really shocked me though was this 20%, about one-in-five Americans with a credit score of 600 or lower.

While you see credit scores rising from 2015 to 2017 for these people with higher scores, those with lower scores are actually seeing their score fall!

And a lot of you are probably sitting there saying, so what. I don’t plan on borrowing any money, I don’t need a credit score if I don’t need a loan.

Please take this seriously because you never know when you’re going to need emergency cash or a loan. The average out-of-pocket for a hospital stay is over $1,100 according to TransUnion and a new transmission for your car will run eight grand.

After destroying my credit score in 2009, I couldn’t get a loan to save my life and it pushed me into cash advances and payday loans costing hundreds in fees. It didn’t end well and I want you to know what I didn’t about your credit score.

What is a Good Credit Score?

But what is a good credit score? What’s the score that will get you the money you need without those double-digit interest rates that break your budget? The rule of thumb is that any score over 670 FICO is good even though rates don’t start going down much until you get a score of 720 or higher.

Anything below 600 FICO is getting bad and we saw how people with bad credit are getting shut out, seeing their score fall over the last few years.

There’s actually a reason for this 670 cutoff for what’s considered a good credit score. That’s the score you need for a loan to qualify for federal guarantees and other programs.

Most people don’t understand that banks aren’t really in the business of holding your loan. Banks are in the business of making loans so what they’ll do is sell the loans to investors for the cash to make more loans. Now being able to sell those loans is a lot easier if the loan qualifies for some federal program or guarantee so banks don’t want to make loans to borrowers with a credit score under 680 FICO.

But that means nearly four-in-ten people are shut out of the financial system with a credit score below that prime lending cutoff. Worse is the one-in-five in that bad credit score range where you can’t even look at a loan for less than 30% interest.

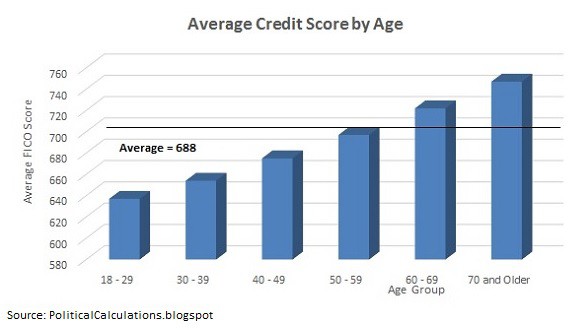

And bad credit isn’t always your fault. This graphic shows the average credit score by age group and because a lot of your credit score revolves around things like credit history and account age, millennials are just getting screwed.

The average FICO score is around 630 for people under 29 years old. That’s well into that bad credit range where you’re locked out of the system and way below the average of 688 FICO for all Americans.

Credit Score Needed to Buy a House

Now you know what’s considered good credit and bad, but what kind of a credit score do you really need for some of life’s major decisions? What credit score do you need to buy a house or a car?

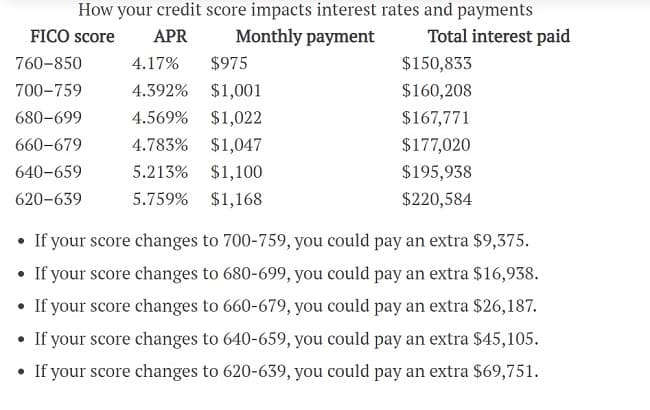

TransUnion ran the numbers for different credit scores on a 30-year mortgage for $200,000 and found a cutoff around 620 FICO for loans. That’s not all though, it’s not just that you’ll have trouble getting a loan with a credit score under 620 but the extra cost you’ll pay if you can get a loan.

That 620 credit score means you pay a rate of 5.75%, more than a percent and a half higher than someone with a FICO of 760 or higher. You’d also be paying almost $200 more a month and nearly $70,000 more in interest over the life of that loan.

Credit Score Needed to Buy a Car

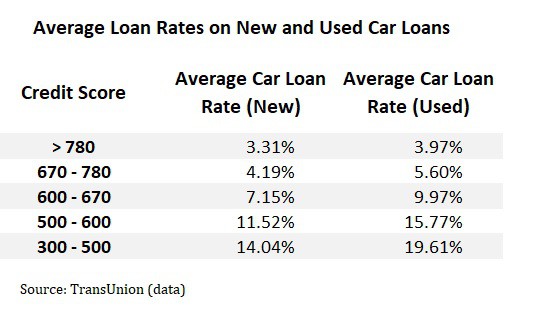

It gets worse for car loans. The rate on a loan for a used car averages almost 20% if your credit score is below 500 FICO. That’s five-times the rate someone pays on good credit and could mean the difference between paying off your car and repossession.

How to Get a Good Credit Score

Now that we know what a good credit score looks like and the score you need, the question is, “How do you increase your credit score?” How do you save that $70,000 on your mortgage by getting good credit?

Here I want to share three tricks I guarantee you haven’t heard. We’ve all heard that you can get bad marks knocked off your credit report and that a limit increase will increase your score.

These three credit score tips are different though. I had never heard of them until a few months ago but was shocked at how fast they actually worked.

Our first credit score hack is to get missing accounts added to your credit reports.

Most people know that you can write the credit bureaus to get things removed from your credit report that shouldn’t be there. This is usually like late payments or bad marks hurting your score.

But what about the good stuff that isn’t on your reports? The bills you pay every month that aren’t on your credit reports and helping your score?

Now creditors don’t have to report your account to the credit bureaus so sometimes they don’t. Most often, this includes things like your utility bill, cable TV and rent is another really common one.

Since payment history is as much as 35% of your credit score, getting these accounts and those regular on-time payments added to your report can be a huge boost. Better still, the change is almost immediate and it can help make your report look better if it has a few bad marks.

So what you want to do here is to contact all the people you’re paying monthly that don’t report on your credit. If you can get them to start reporting, it’s an instant win.

The phone company and cable usually won’t report but you can get your landlord to start reporting rent through sites like PayYourRent and Rental Kharma which even allows you to add past rent history.

Next here to increase your credit score is to pay your card balance before it’s reported to the credit bureaus.

Even if you’re paying your credit card balance in full each month, it might be getting reported that you have a balance on your credit report. This is because card companies don’t always report balances after your due date for the payment.

In fact, most card companies report balances to the credit bureaus at the end of the month. It’s after your monthly statement has closed for that month but before the payment is due.

For example, Barclays closes my statement on the 24th of the month but the payment isn’t due until the 13th of the next month. I pay it down to zero every month before it’s due but was surprised when I looked at my credit report and it showed I was carrying a balance.

The problem was that Barclays reports balances to the credit bureaus at the end of the month, after my statement closes but before the payment due date. So even though I was paying my card off, it was still showing a balance on my credit report every month and hurting my credit score.

This one’s an easy fix though. Just call your credit card customer support and find out what date they report to the credit bureaus. You can usually get your payment due date switched to before this date or just make it a point to pay off your card before they report.

Another credit hack you can try is to pay off your highest balance cards first.

Now I’m one of the biggest proponents of the debt snowball method. That’s where you rank your debts by amount and then make extra payments to the smaller ones first. It’s a great motivator because you see those smaller bills dropping off your list faster.

The problem is, it’s not the best for your credit or your checkbook.

Those bigger debts, especially the credit card balances, hurt your FICO score more because of what’s called the credit utilization ratio. This is the amount you owe on each debt versus your credit limit. So if you owe $8,000 on a card with a $10,000 limit, your utilization ratio is 80% which is really high.

A higher utilization ratio, so owing up to the limits on your cards or other revolving debt, is a sign of being overextended and a big warning for creditors.

Paying down those bigger card balances first is going to lower your utilization ratio and it might save you money as well if those higher balances happen to be on higher-rate debt.